Ex 2: Recruitment linked to an environmental covariate (Cold Pool Index)

Source:vignettes/ex02_CPI_recruitment.Rmd

ex02_CPI_recruitment.RmdIn this vignette we walk through an example using the

wham (WHAM = Woods Hole Assessment Model) package to run a

state-space age-structured stock assessment model. WHAM is a

generalization of code written for Miller et al. (2016)

and Xu et

al. (2018), and in this example we apply WHAM to the same stock,

Southern New England / Mid-Atlantic Yellowtail Flounder.

This is the 2nd wham example, which builds off model

m4 from example 1 (full state-space model, numbers at all

ages are random effects, logistic normal age-compositions). We assume

you already have wham installed. If not, see the Introduction. The simpler

1st example, without environmental effects, is available as a R

script and vignette.

In example 2, we demonstrate how to specify and run WHAM with varying

recruitment models (random, Bev-Holt, Ricker)

environmental covariate (Cold Pool Index, CPI) process models (random walk, AR1), and

how the CPI affects recruitment (controlling or limiting)

As in example

1, we check that each model converges

(check_convergence()), plot diagnostics, results, and

reference points (plot_wham_output()), and compare models

using AIC and Mohn’s rho (compare_wham_models()).

1. Prepare wham

Open R and load the wham package:

For a clean, runnable .R script, look at

ex2_CPI_recruitment.R in the example_scripts

folder of the wham package. You can run this entire example

script with:

wham.dir <- find.package("wham")

source(file.path(wham.dir, "example_scripts", "ex2_CPI_recruitment.R"))Let’s create a directory for this analysis:

# choose a location to save output, otherwise will be saved in working directory

write.dir <- "choose/where/to/save/output" #e.g., tempdir(check=TRUE)

dir.create(write.dir)

setwd(write.dir)WHAM was originally built by modifying the ADMB-based ASAP model code

(Legault

and Restrepo 1999), and is designed to take an ASAP3 .dat file as

input. We generally assume in wham that you have an

existing ASAP3 .dat file. If you are not familiar with ASAP3 input

files, see the ASAP documentation

and code. For this

vignette, an example ASAP3 input file is provided,

ex2_SNEMAYT.dat. We will also need a data file with an

environmental covariate, the Cold Pool Index, CPI.csv.

Read in ex2_SNEMAYT.dat and CPI.csv to

R:

wham.dir <- find.package("wham")

asap3 <- read_asap3_dat(file.path(wham.dir,"extdata","ex2_SNEMAYT.dat"))

env.dat <- read.csv(file.path(wham.dir,"extdata","CPI.csv"), header=T)We generally abbreviate ‘environmental covariate’ as

ecov in the code. In this example, the ecov

data file has columns for observations (CPI), standard

error (CPI_sigma), and year (Year).

Observations and year are always required. Standard error can be treated

as fixed/data with yearly values (as here) or one overall value shared

among years. It can also be estimated as a parameter(s), likewise either

as yearly values or one overall value.

head(env.dat)

#> Year CPI CPI_sigma

#> 1 1973 0.5988 0.2838

#> 2 1974 -0.1760 0.2465

#> 3 1975 -1.1887 0.2539

#> 4 1976 -0.7938 0.2634

#> 5 1977 -0.6771 0.1576

#> 6 1978 -1.5195 0.20452. Specify models

Now we specify how the 7 models treat recruitment, the CPI process, and how the CPI affects recruitment:

Ecov_how <- paste0(

c("none", "controlling-", "none", "limiting-", "limiting-", "controlling-", "controlling-"),

c("", "lag-1-", "", rep("lag-1-",4)),

c("", "linear", "", rep("linear", 4)))

df.mods <- data.frame(Recruitment = c(2,2,3,3,3,3,4),

Ecov_process = c(rep("rw",4),rep("ar1",3)),

Ecov_how = Ecov_how, stringsAsFactors=FALSE)

n.mods <- dim(df.mods)[1]

df.mods$Model <- paste0("m",1:n.mods)

df.mods <- dplyr::select(df.mods, Model, tidyselect::everything()) # moves Model to first colLook at the model table. The Ecov_how is a a more recent

character string approach to defining environmental effects on

recruitment.

df.mods

#> Model Recruitment Ecov_process Ecov_how

#> 1 m1 2 rw none

#> 2 m2 2 rw controlling-lag-1-linear

#> 3 m3 3 rw none

#> 4 m4 3 rw limiting-lag-1-linear

#> 5 m5 3 ar1 limiting-lag-1-linear

#> 6 m6 3 ar1 controlling-lag-1-linear

#> 7 m7 4 ar1 controlling-lag-1-linearWe specify the options for modeling recruitment and any environmental

covariate(s) using the prepare_wham_input() function. WHAM

provides 4 options for recruitment (recruit_model):

- random walk,

- random about mean,

- Beverton-Holt, and

- Ricker.

The environmental covariate options are fed to

prepare_wham_input() as a list, ecov:

m=1 # example for first model

ecov <- list(

label = "CPI",

mean = as.matrix(env.dat$CPI),

logsigma = as.matrix(log(env.dat$CPI_sigma)),

year = env.dat$Year,

use_obs = matrix(1, ncol=1, nrow=dim(env.dat)[1]), # use all obs (=1)

process_model = df.mods$Ecov_process[m], # "rw" or "ar1"

recruitment_how = matrix(df.mods$Ecov_how[m],1,1)) #matrix for number of stocks (1) and number of Ecovs (1)There are currently 2 options for the ecov process model

(ecov$process_model): 1) random walk ('rw'),

and 2) autoregressive ('ar1'). Recent versions of WHAM now

specify effects of covariates on recruitment, natural mortality,

catchability, and movement using character strings. For recruitment we

specify recruitment_how for the mechanistic affect on

recruitment, the time lag between the covariate and recruitment, and the

order of the orthogonal polynomial effect. The options for the

mechanistic effect follow Iles

and Beverton (1998) and Xu et

al. (2018):

- “controlling” (density-independent mortality),

- “limiting” (carrying capacity, e.g.

ecovdetermines amount of suitable habitat), - “lethal” (threshold, i.e. R –> 0 at some

ecovvalue),

- “masking” (metabolic/growth,

ecovdecreases dR/dS), and - “directive” (e.g., behavioral).

In Ecov_how we specify the lag of 1 for

the CPI so that CPI in year t affects recruitment in year t

+ 1. We also specify a first order polynomial (“linear” or

“poly-1”). For no effect of the covariate, but still keeping the

state-space model estimation for the covariate, Ecov_how=

“none”.

You can set ecov = NULL or process_model=

NA to fit the model without environmental covariate data, but note that

here we fit the ecov data even for models without an

ecov effect on recruitment (m1 and

m3) so that we can compare them via AIC (need to have the

same data in the likelihood).

Options are described in the set_ecov help page. Not all

mechanistic effects options are implemented for every recruitment

model.

?set_ecov3. Run the models

for(m in 1:n.mods){

# set up environmental covariate data and model options

ecov <- list(

label = "CPI",

mean = as.matrix(env.dat$CPI),

logsigma = as.matrix(log(env.dat$CPI_sigma)),

year = env.dat$Year,

use_obs = matrix(1, ncol=1, nrow=dim(env.dat)[1]), # use all obs (=1)

process_model = df.mods$Ecov_process[m], # "rw" or "ar1"

recruitment_how = matrix(df.mods$Ecov_how[m],1,1)) #matrix for number of stocks (1) and number of Ecovs (1)

# (not used in this vignette) can set ecov = NULL to fit model without ecov data

if(is.na(df.mods$ecov_process[m])) ecov = NULL

# generate wham input from ASAP3 and ecov data

input <- prepare_wham_input(asap3, recruit_model = df.mods$Recruitment[m],

model_name = "Ex 2: SNEMA Yellowtail Flounder with CPI effects on R",

ecov = ecov,

NAA_re = list(sigma="rec+1", cor="iid"),

age_comp = "logistic-normal-pool0") # logistic normal pool 0 obs

# Selectivity = logistic, not age-specific as in ex1

# 2 pars per block instead of n.ages

# sel pars of indices 4/5 fixed at 1.5, 0.1 (specified via neg phase in ex2_SNEMAYT.dat)

input$par$logit_selpars[1:4,7:8] <- 0 # last 2 rows will not be estimated (mapped to NA)

# Fit model

mod <- fit_wham(input, do.retro=TRUE, do.osa=TRUE)

# Save model

saveRDS(mod, file=paste0(df.mods$Model[m],".rds"))

# Plot output in new subfolder

plot_wham_output(mod=mod, dir.main=file.path(getwd(),df.mods$Model[m]), out.type='html')

}4. Check for convergence

Collect all models into a list.

We need to check that the models converged. The maximum absolute

gradient should be very close to 0 and SE estimates should be calculable

(invertible Hessian, TMB::sdreport() succeeds). All models

seem to have converged and have a positive definite Hessian.

vign2_conv <- lapply(mods, function(x) capture.output(check_convergence(x)))

for(m in 1:n.mods) cat(paste0("Model ",m,":"), vign2_conv[[m]], "", sep='\n')#> Model 1:

#> stats:nlminb thinks the model has converged: mod$opt$convergence == 0

#> Maximum gradient component: 1.74e-10

#> Max gradient parameter: logit_selpars

#> TMB:sdreport() was performed successfully for this model

#>

#> Model 2:

#> stats:nlminb thinks the model has converged: mod$opt$convergence == 0

#> Maximum gradient component: 1.88e-10

#> Max gradient parameter: logit_selpars

#> TMB:sdreport() was performed successfully for this model

#>

#> Model 3:

#> stats:nlminb thinks the model has converged: mod$opt$convergence == 0

#> Maximum gradient component: 4.17e-10

#> Max gradient parameter: logit_selpars

#> TMB:sdreport() was performed successfully for this model

#>

#> Model 4:

#> stats:nlminb thinks the model has converged: mod$opt$convergence == 0

#> Maximum gradient component: 1.35e-10

#> Max gradient parameter: logit_selpars

#> TMB:sdreport() was performed successfully for this model

#>

#> Model 5:

#> stats:nlminb thinks the model has converged: mod$opt$convergence == 0

#> Maximum gradient component: 1.45e-10

#> Max gradient parameter: logit_selpars

#> TMB:sdreport() was performed successfully for this model

#>

#> Model 6:

#> stats:nlminb thinks the model has converged: mod$opt$convergence == 0

#> Maximum gradient component: 1.34e-10

#> Max gradient parameter: logit_selpars

#> TMB:sdreport() was performed successfully for this model

#>

#> Model 7:

#> stats:nlminb thinks the model has converged: mod$opt$convergence == 0

#> Maximum gradient component: 1.72e-10

#> Max gradient parameter: logit_selpars

#> TMB:sdreport() was performed successfully for this model5. Compare models

Let’s first make the results table prettier.

df.mods$Recruitment <- dplyr::recode(df.mods$Recruitment, `2`='Random', `3`='Bev-Holt', `4`='Ricker')

df.mods$Ecov_how <- c("---", "Controlling", "---", "Limiting", "Limiting", "Controlling", "Controlling")Now get the convergence information.

opt_conv = 1-sapply(mods, function(x) x$opt$convergence)

ok_sdrep = sapply(mods, function(x) if(x$na_sdrep==FALSE & !is.na(x$na_sdrep)) 1 else 0)

df.mods$conv <- as.logical(opt_conv)

df.mods$pdHess <- as.logical(ok_sdrep)

df.mods$NLL <- sapply(mods, function(x) round(x$opt$objective,3))Only calculate AIC and Mohn’s rho for converged models.

not_conv <- !df.mods$conv | !df.mods$pdHess

mods2 <- mods

mods2[not_conv] <- NULL

df.aic.tmp <- as.data.frame(compare_wham_models(mods2, table.opts=list(sort=FALSE, calc.rho=T))$tab)

df.aic <- df.aic.tmp[FALSE,]

ct = 1

for(i in 1:n.mods){

if(not_conv[i]){

df.aic[i,] <- rep(NA,5)

} else {

df.aic[i,] <- df.aic.tmp[ct,]

ct <- ct + 1

}

}

df.mods <- cbind(df.mods, df.aic)

df.mods <- df.mods[order(df.mods$dAIC, na.last=TRUE),]

df.mods[is.na(df.mods$AIC), c('dAIC','AIC','rho_R','rho_SSB','rho_Fbar')] <- "---"

rownames(df.mods) <- NULLPrint and save the results table. m6 has the lowest AIC

(Bev-Holt recruitment, CPI modeled as AR1, controlling effect of CPI on

recruitment), but m5 and m7 have similar AIC

values.

df.mods

save(df.mods, file="vign2_res.RData")#> Recruitment Ecov_process Ecov_how Model conv pdHess NLL Rsig dAIC

#> 1 Bev-Holt ar1 Controlling m6 TRUE TRUE -824.765 0.688 0.0

#> 2 Bev-Holt ar1 Limiting m5 TRUE TRUE -824.272 0.694 1.0

#> 3 Ricker ar1 Controlling m7 TRUE TRUE -824.250 0.699 1.0

#> 4 Bev-Holt rw Limiting m4 TRUE TRUE -813.544 0.693 20.4

#> 5 Random rw Controlling m2 TRUE TRUE -810.097 0.780 25.3

#> 6 Bev-Holt rw --- m3 TRUE TRUE -808.177 0.859 29.1

#> 7 Random rw --- m1 TRUE TRUE -803.139 0.997 37.2

#> AIC rho_R rho_SSB rho_Fbar

#> 1 -1509.5 0.2072 0.1070 -0.1334

#> 2 -1508.5 0.2152 0.1126 -0.1382

#> 3 -1508.5 0.2044 0.1030 -0.1302

#> 4 -1489.1 0.2149 0.1129 -0.1384

#> 5 -1484.2 0.2312 0.1196 -0.1459

#> 6 -1480.4 0.2319 0.1094 -0.1351

#> 7 -1472.3 0.2592 0.1169 -0.14526. Results

There are various options for creating WHAM output. The default is to

create a self-contained html file using Rmarkdown and individual plot

files (.png) that are organised within subdirectories of

plots_png. The html file also includes tables of estimates

for fundamental parameters and abundance and fishing mortality at age.

On Windows you may need to use Chrome or Internet Explorer to view the

.html (there have been issues using Firefox on Windows but

not Linux).

# save output plots in subfolder for each model

for(m in 1:n.mods) plot_wham_output(mod=mods[[m]], dir.main=file.path(getwd(), df.mods$Model[m]), out.type='html')Cold Pool Index (CPI)

Models that included an effect of the Cold Pool Index on recruitment

were strongly supported by AIC over models without CPI effects

(m2 and m4-7 lower AIC than m1

and m3). Note that we can compare models with and without a

CPI effect on recruitment using AIC because we also fit the CPI data in

the models without the effect (m1 and m3).

Comparing m4 and m5 demonstrates that the

CPI was best modeled as an AR1 process (m5) instead of a

random walk (m4), since this was the only difference

between the two models and m5 had lower AIC. The

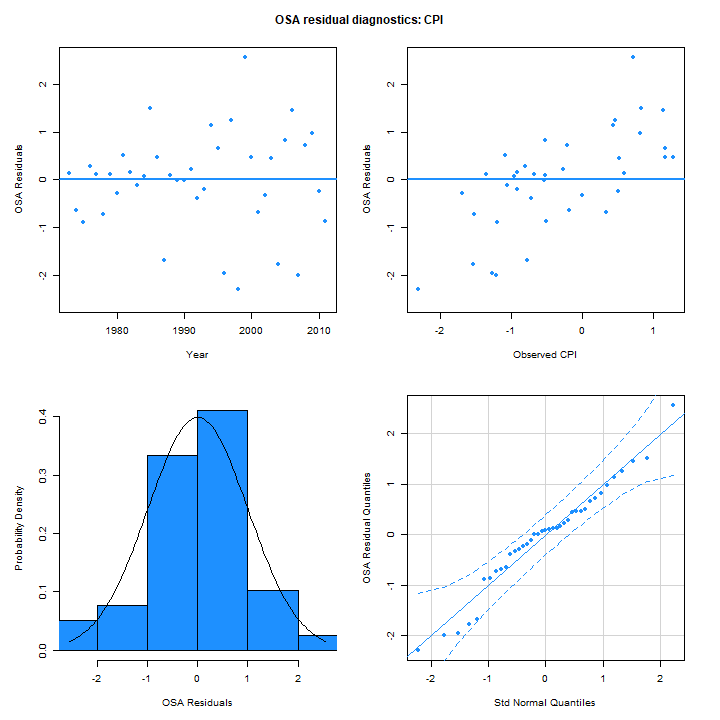

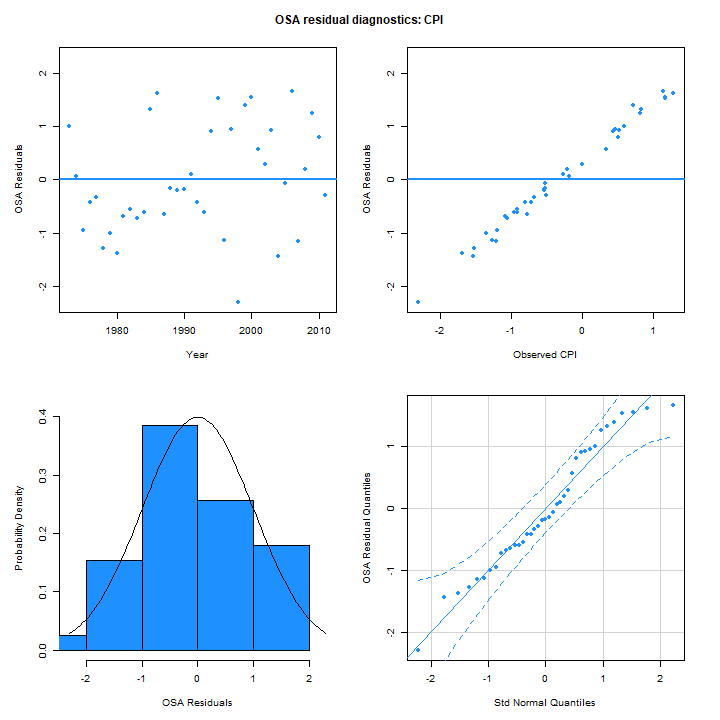

one-step-ahead residuals for the CPI from m5 (right) are

similar in distribution. The linear trend in the OSA residuals with

observed value for m5 is due to the best prediction of the

next observation being near the mean of the process in this case because

the estimated autocorrelation parameter is near 0:

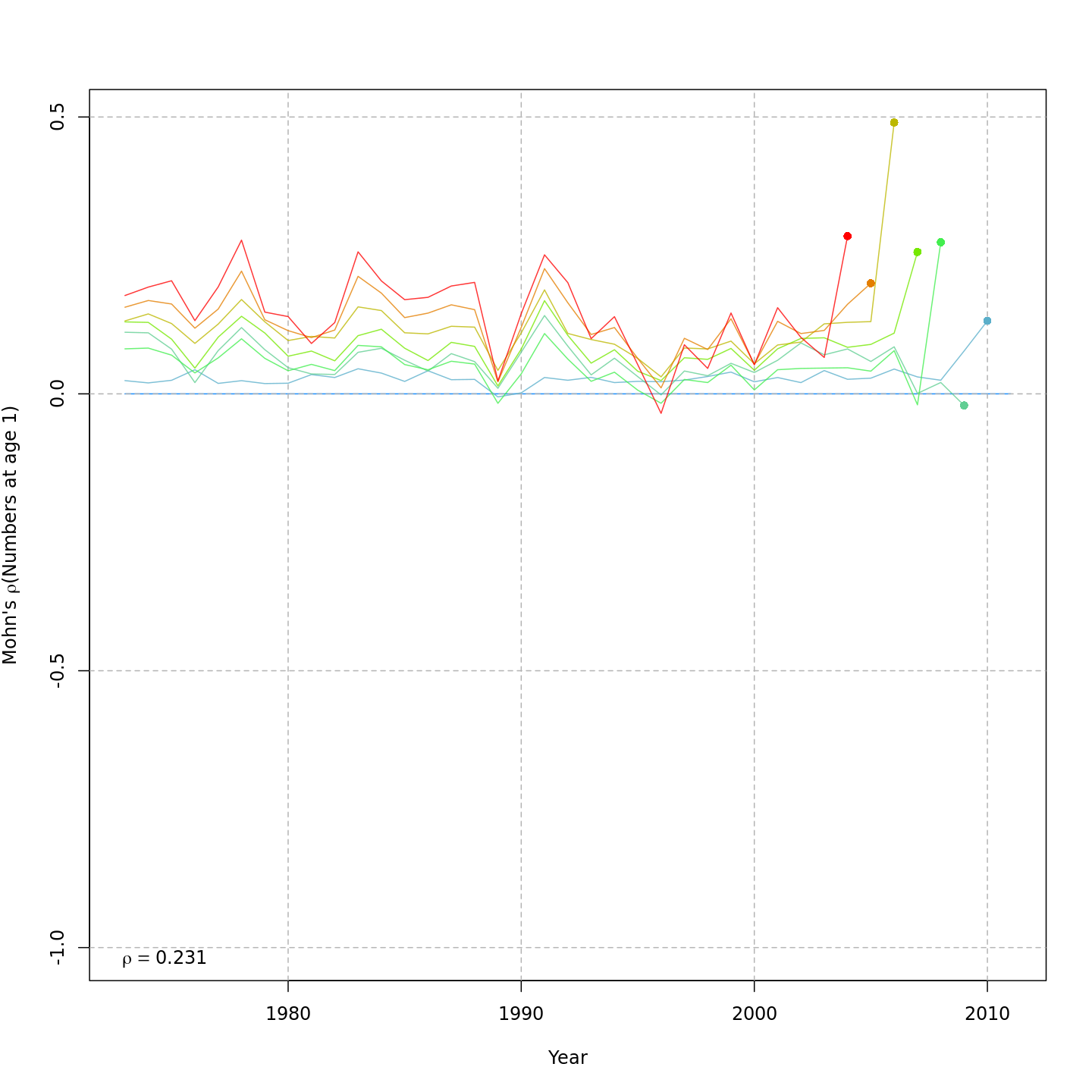

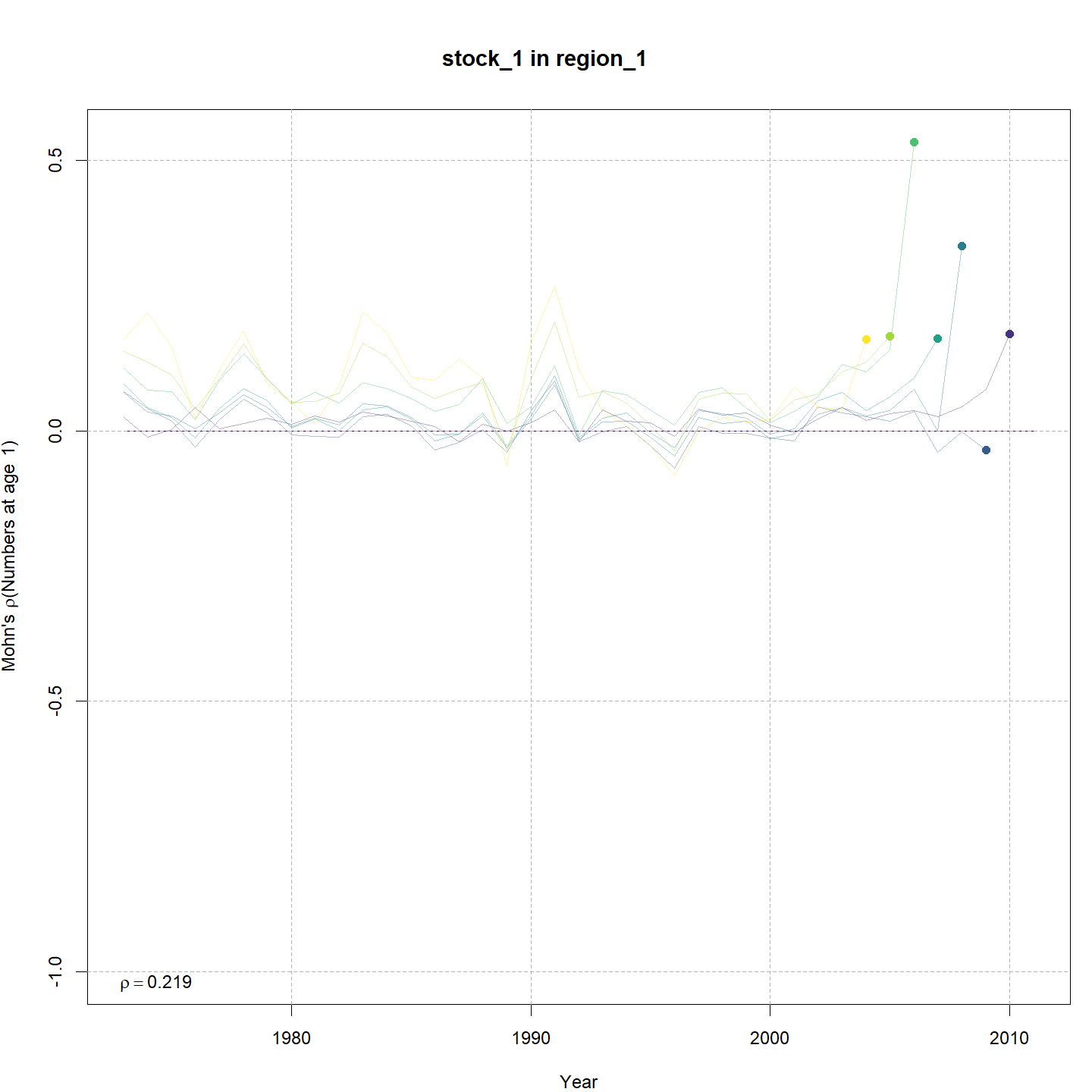

As we saw from the table of results, all the models produced similar

Mohn’s

values for SSB, F, and recruitment. Below are the relative retrospective

peels for the model without any SSB or CPI effects on recruitment

(m1, left) and the best model that included CPI and SSB

effects on recruitment, (m6, right).

Recruitment

A Beverton-Holt stock-recruitment assumption was preferred over

random recruitment (m3 lower AIC than m1).

Models that included both Bev-Holt and CPI effects on recruitment had

lower AIC than the model with Bev-Holt but without the CPI

(m4 vs. m3). Adding the CPI effect to the

Bev-Holt explains some of the variability around the stock-recruit

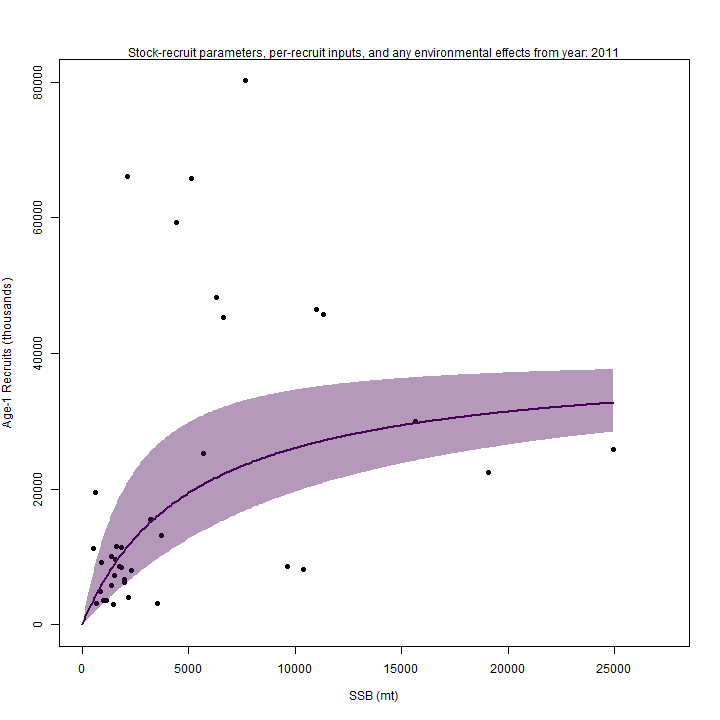

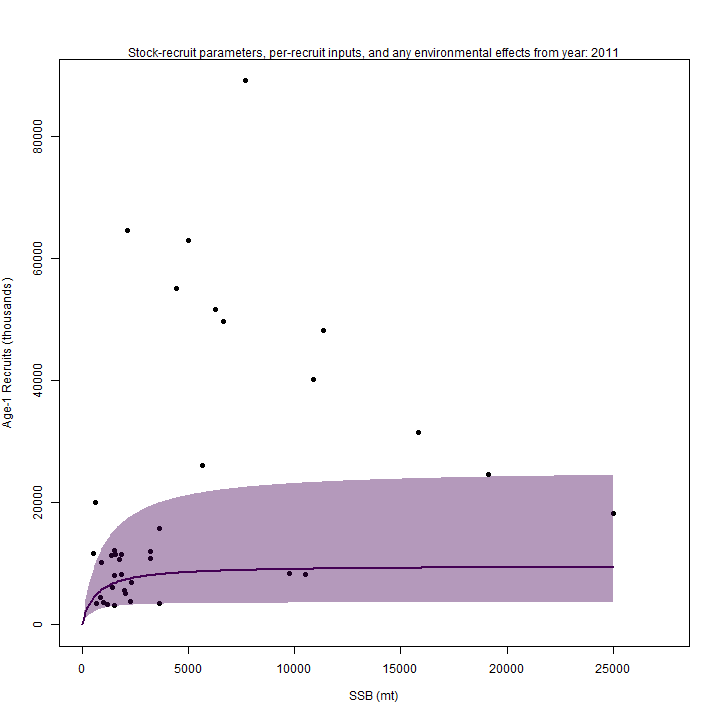

curve, which resulted in m4 (right) estimating lower

than m3 (left).

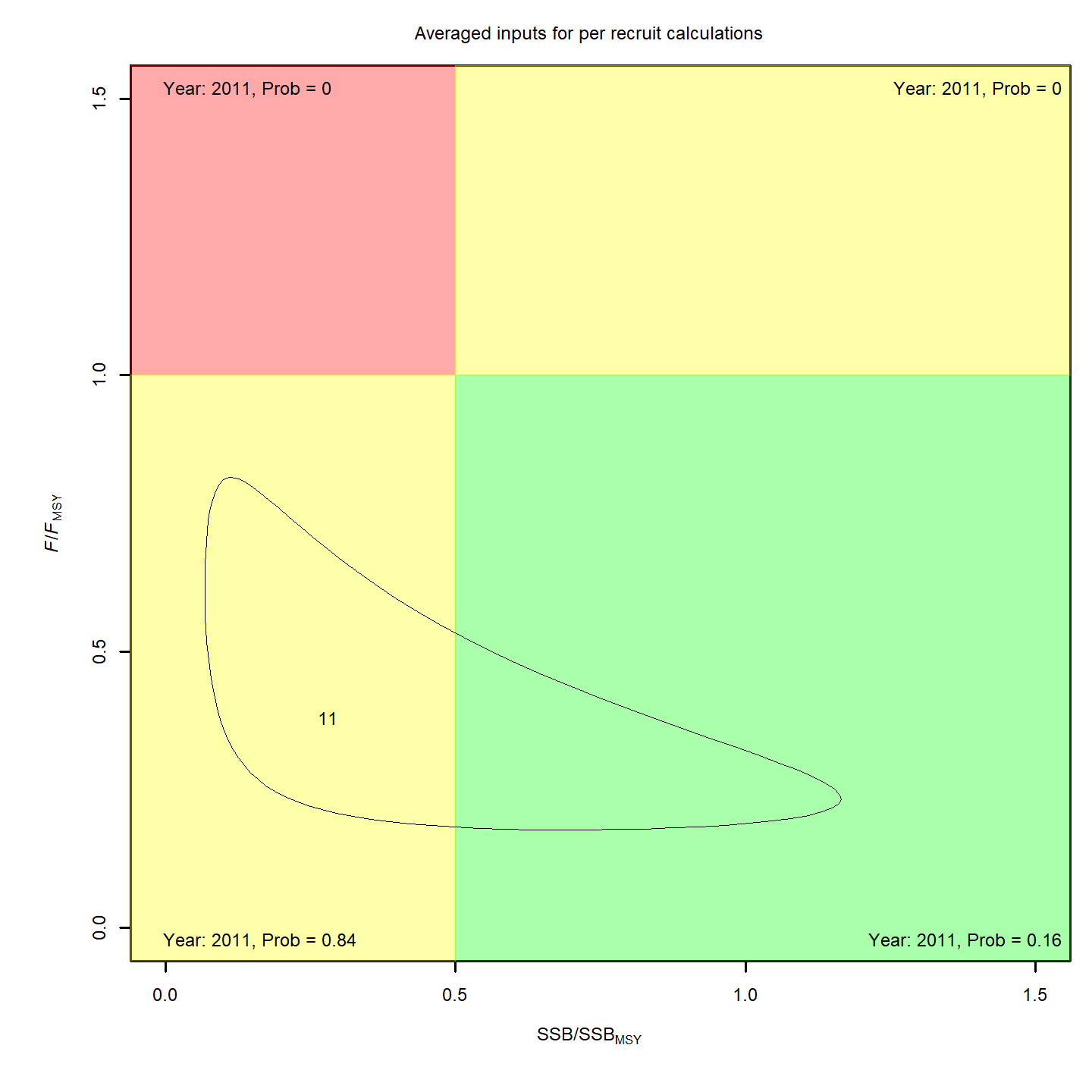

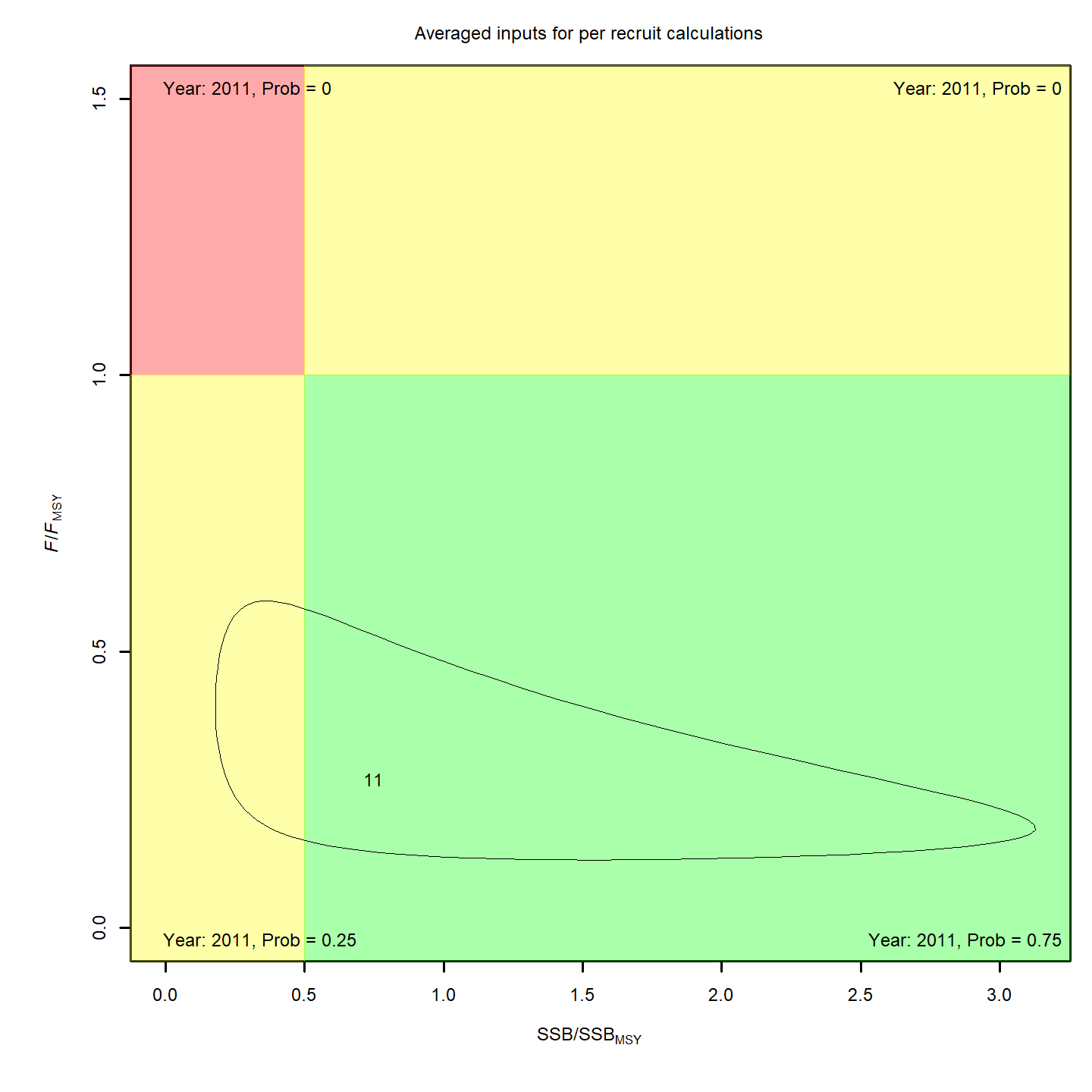

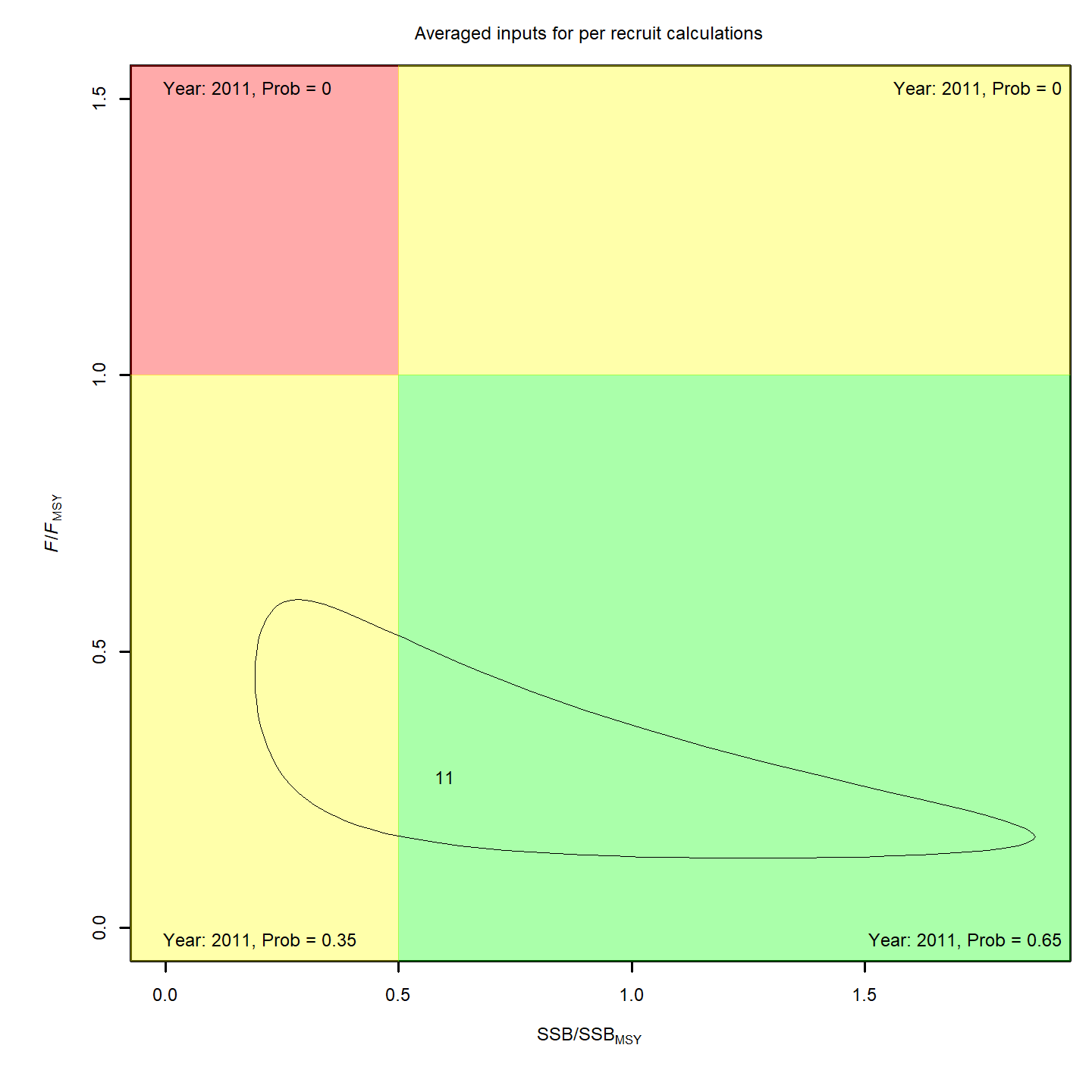

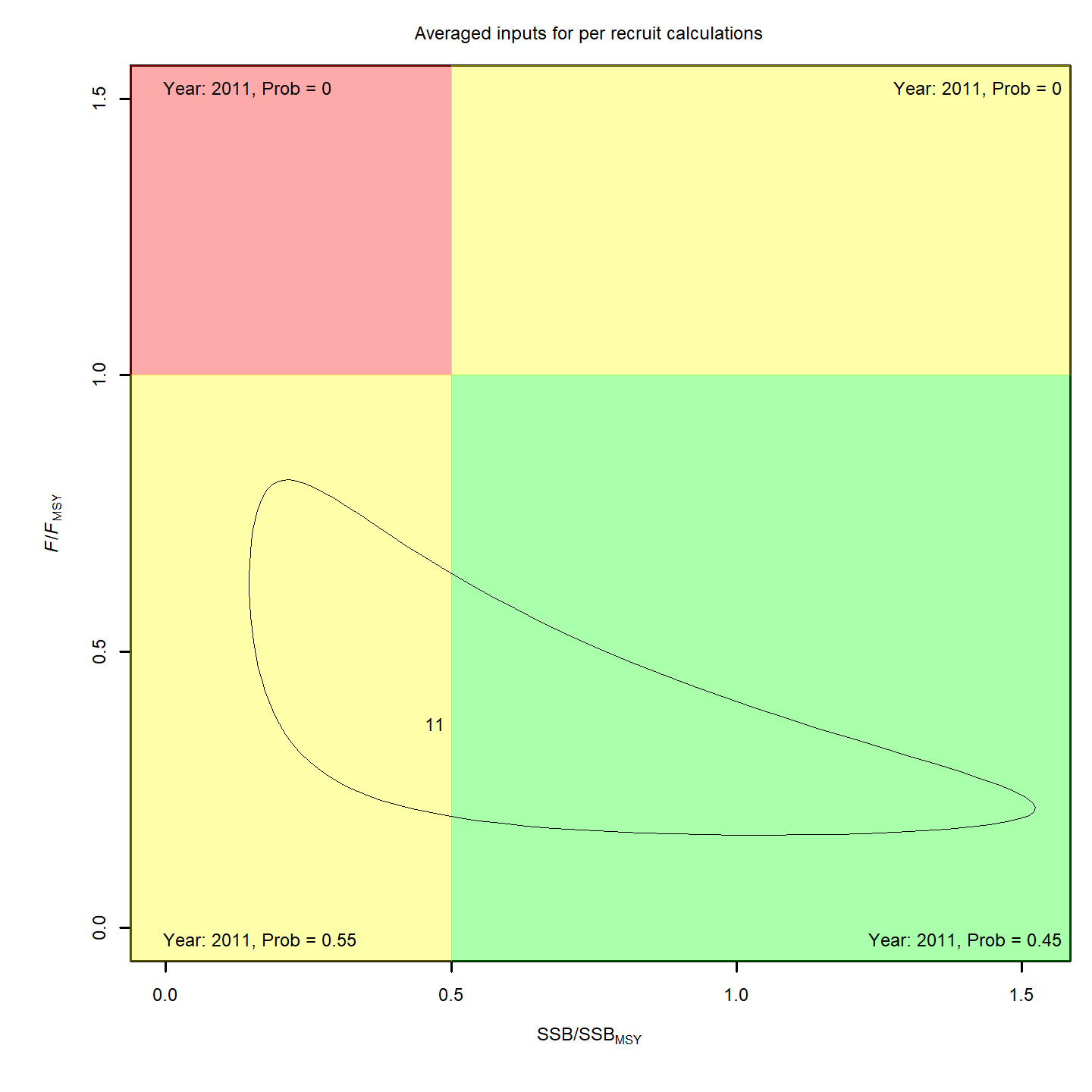

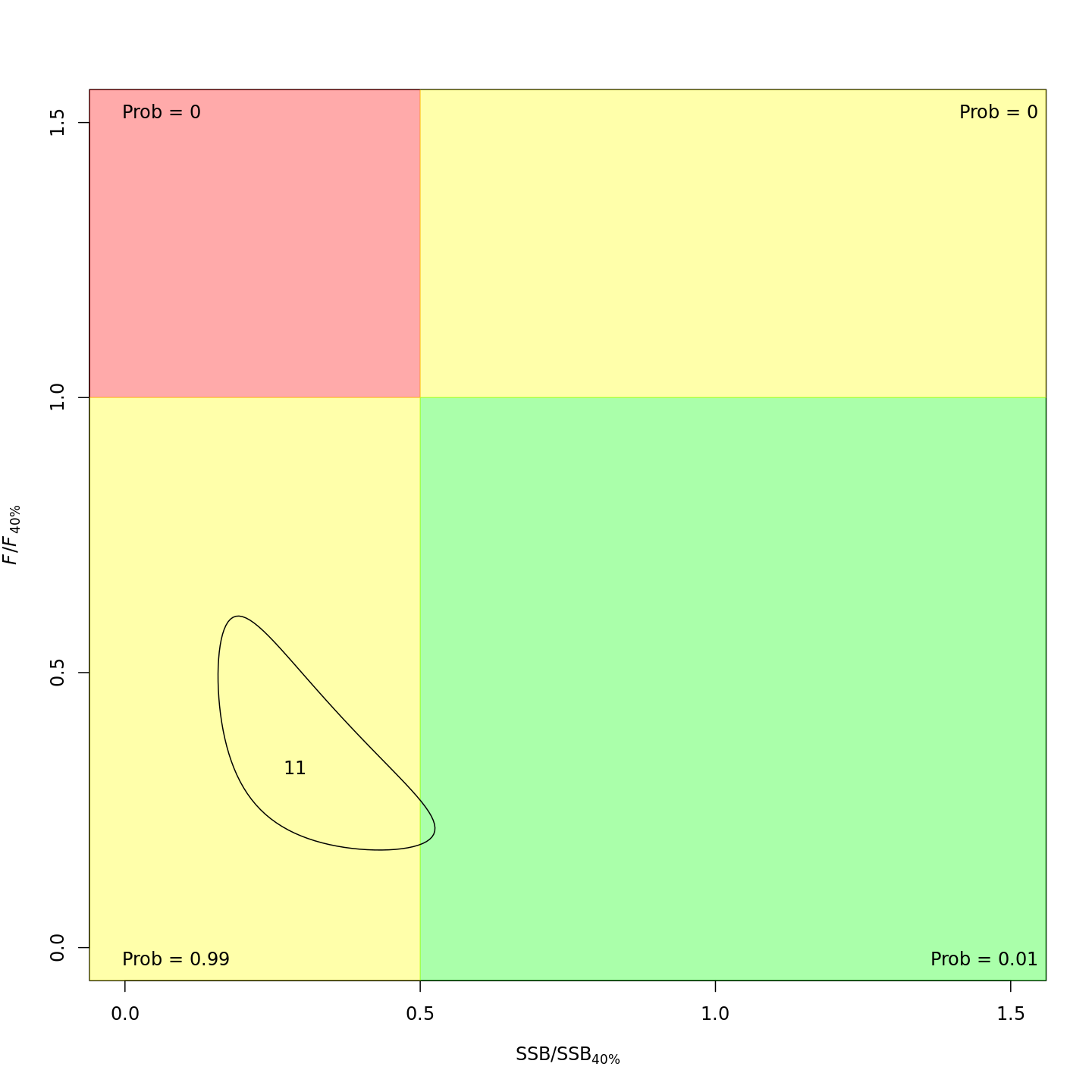

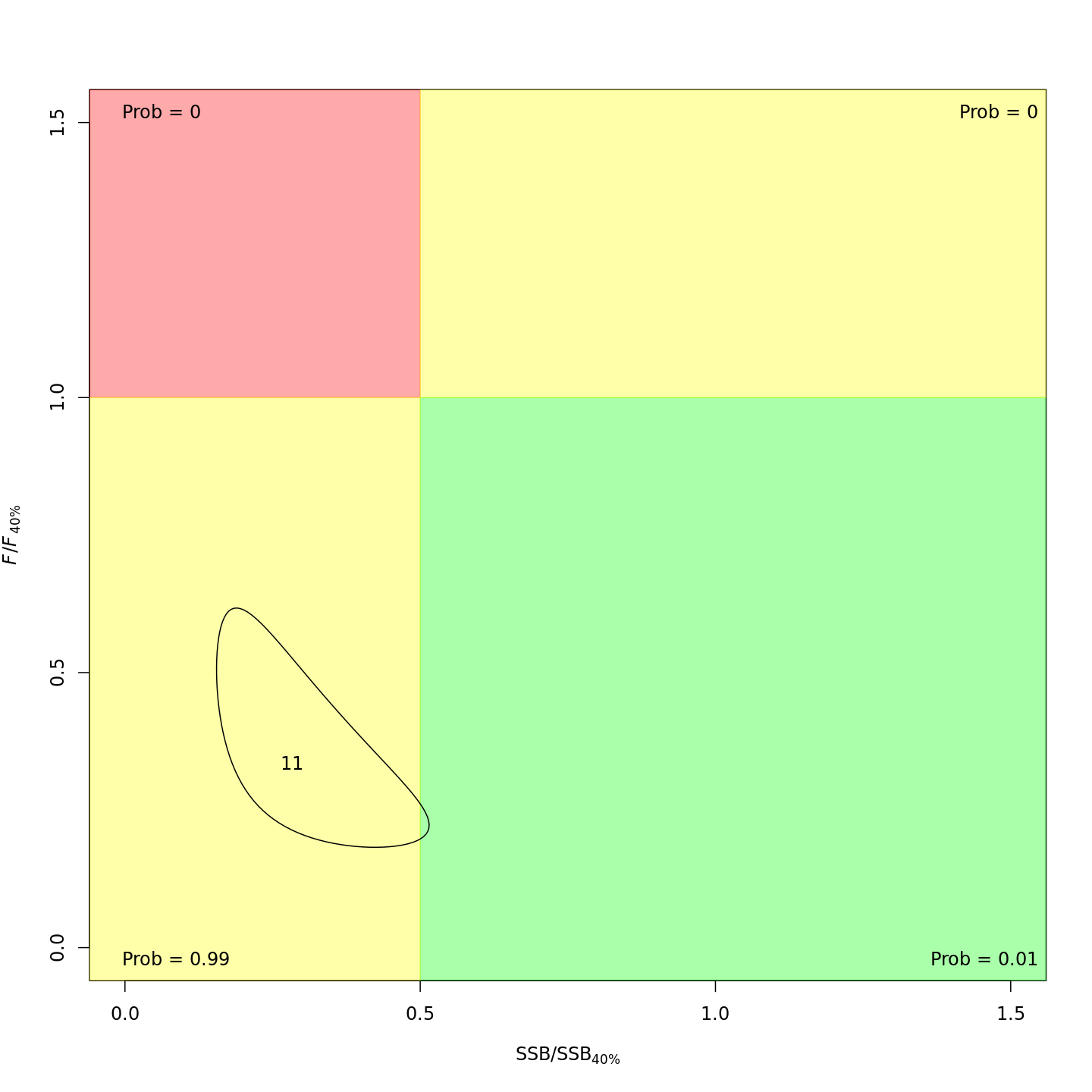

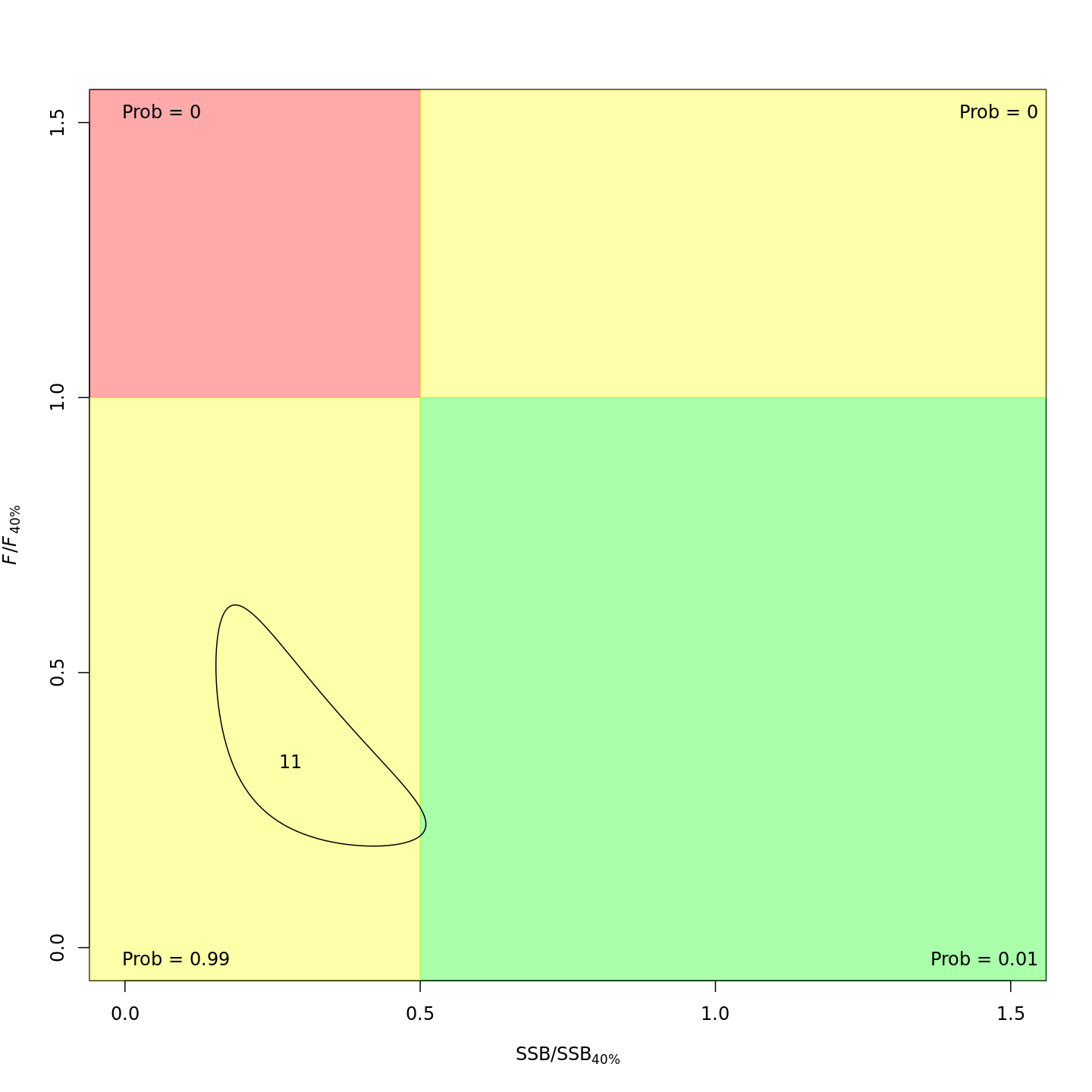

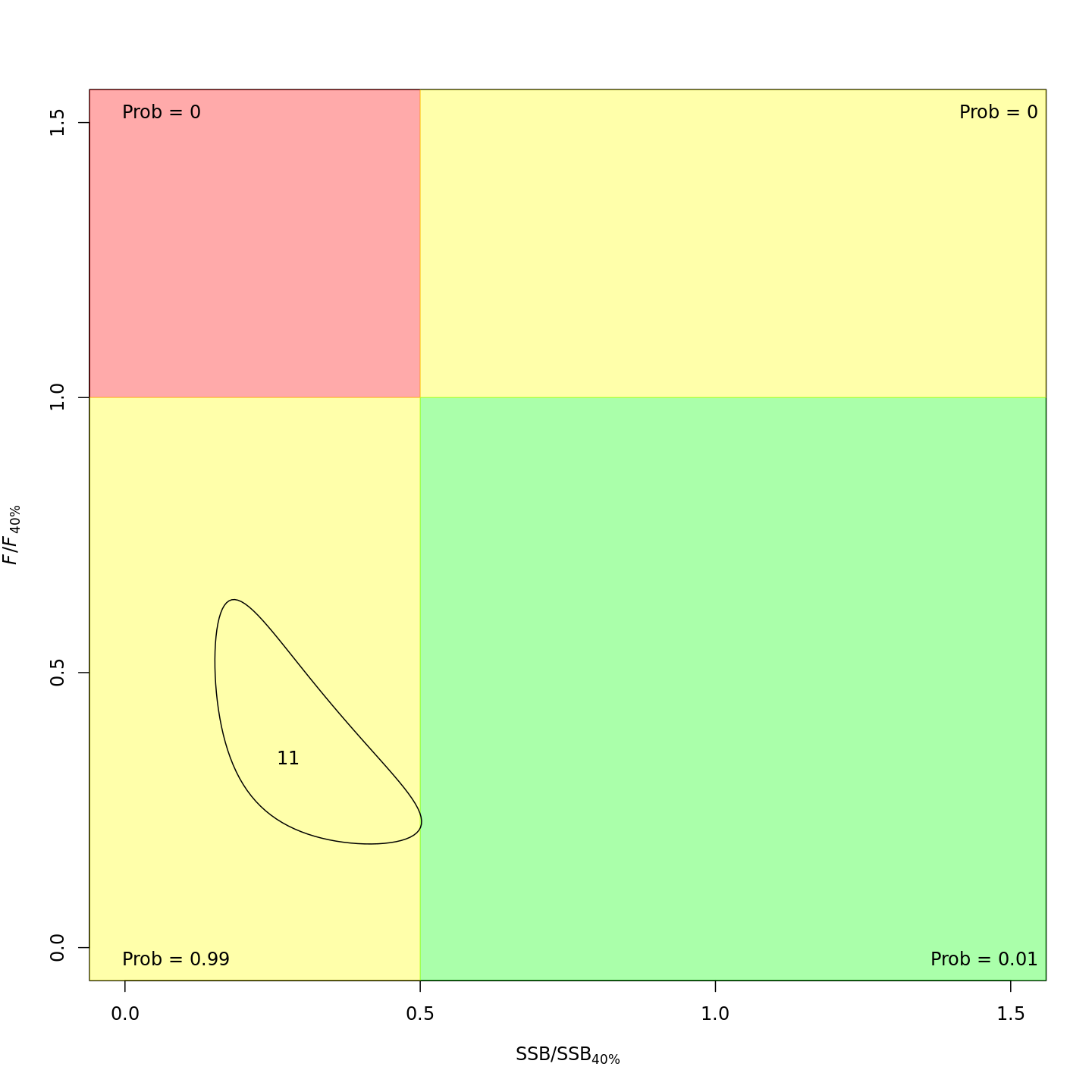

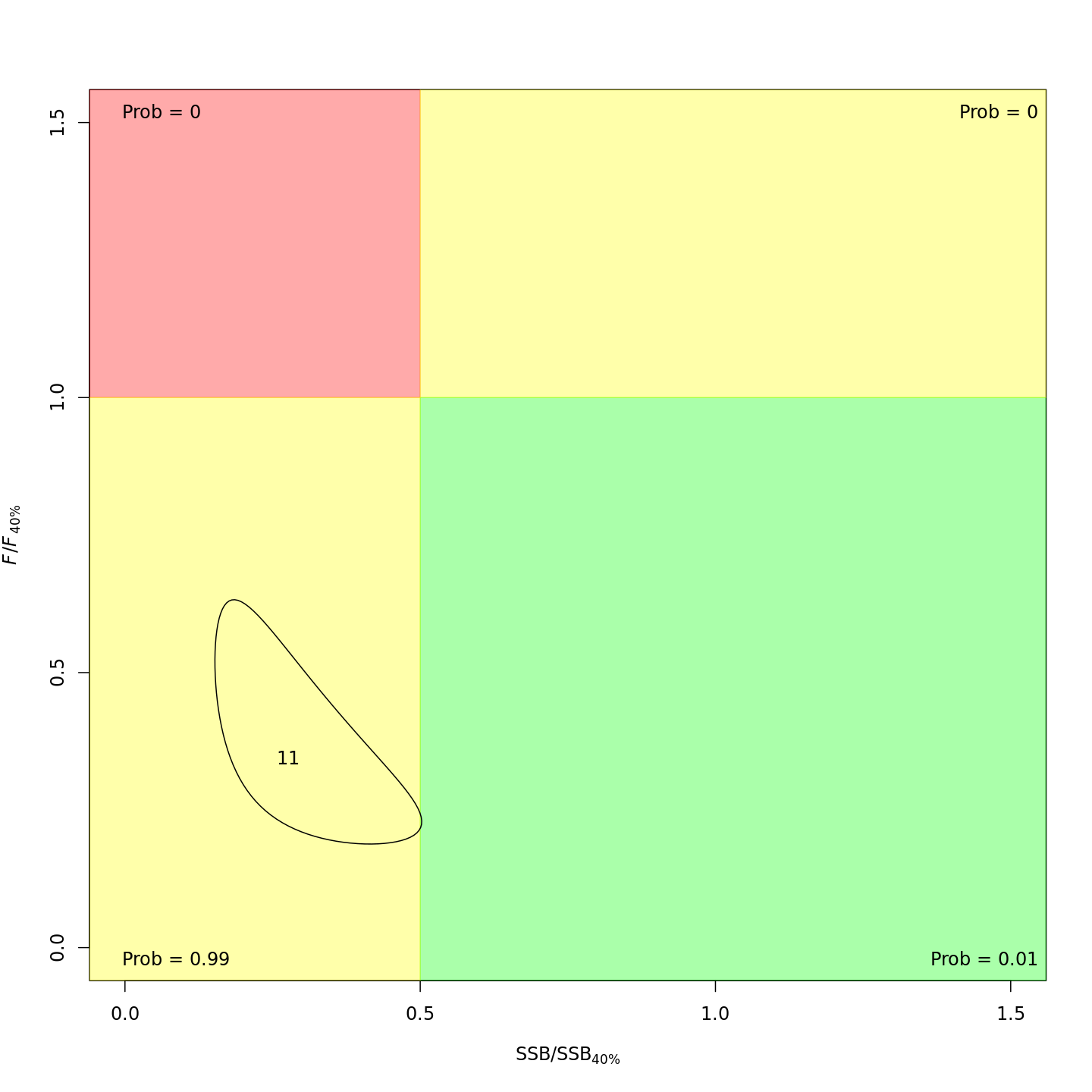

Stock status

Whether or not to include a stock-recruit function and/or the CPI did not have a great influence on estimated stock status using SPR-based reference points. Specifically, the models hardly differed in their estimation of the probability that the stock was overfished, . All models estimated with 100% probability that the stock was not experiencing overfishing in 2011, .

For models with stock recruit functions, status based on MSY-based

reference points is more optimistic: